|

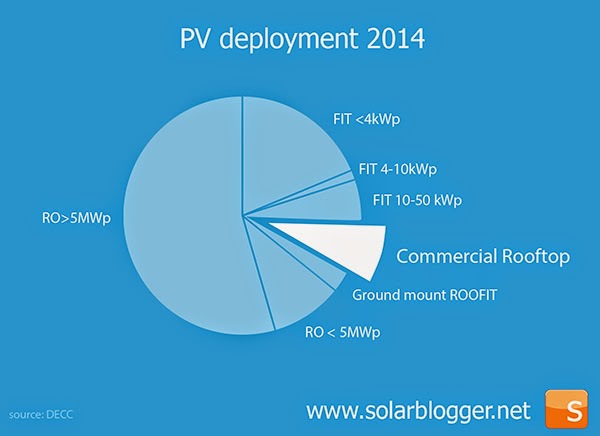

| Commercial Rooftop Solar was only 8% of the Market in 2014 |

It seems to be accepted wisdom that the commercial rooftop

sector is set to be the next big thing in solar. In recent weeks companies more

commonly associated with the solar farm sector such as Lightsource, Conergy and

Lark have announced their intention to develop commercial rooftop divisions.

Indeed, there are good reasons to expect the commercial

rooftop segment to take off. As feed in tariff support has been gradually

withdrawn, the savings on electricity bills become a greater and greater

proportion of the financial justification for solar PV. Unlike the

domestic sector the daytime energy use in office buildings and factories is

well matched to solar energy production.

Unlike ground mounted solar farms, the aesthetics of solar

on factory, warehouse and barn roofs isn’t the least bit controversial.

Even the most virulent strain of Daily Mail journalist couldn’t really

complain about the ‘industrialisation’ of an industrial estate, could

they? Actually, don’t answer that

question, but you get the point.

Commercial rooftops offer installations at a scale to drive

low installation costs. Industrial estates often already have chunky

electricity supplies.

This combination of scale, self-consumption, and relaxed

attitude to aesthetics has created a real sweet spot for solar. Commercial rooftop seems to be the sector

that’s closest to a subsidy-free market.

Despite this, mid-size commercial rooftops (which I've taken as >50kWp FIT

non-standalone) represented only 8% of the PV capacity installed in 2014, far

behind solar farms (assumed to be RO funded) with 64% and domestic scale FIT with 19% of the market. Given all this, it’s hardly surprising that many people have identified

this sector as providing a real opportunity for growth.

The Challenges

For sure, the sector faces challenges. Demanding hurdle rates or payback times are

common for investment decisions in commercial businesses. Making an offer that works for both a

landlord and their tenants and the limitations of our creaky electricity grid

could all be potential barriers to deployment.

However, these challenges are as nothing compared to the

emerging risk to the Feed in Tariff (FIT).

The level of quarterly deployment that triggers a 3.5%

degression to the FIT has been set at 50MWp for systems above 50kWp. This band was recently split into standalone

systems and systems supplying buildings.

The trigger level for systems supplying buildings has reduced to 32.5

MWp going forward, an annual deployment level of 130MWp.

The graph shows deployment for the combined segment, which

has risen from 2012 to breach the degression trigger twice in the last four

quarters.

|

| The FIT depression cap has already been breached in 2 of the last 4 quarters |

The companies piling into the commercial rooftop sector are refugees from a solar farm sector brutally cut back by the government. In 2014 solar farms accounted for nearly two

thirds of all solar PV installed in the UK.

1,100 MWp was installed in farms larger than 5MWp and a further 200MWp in farms smaller than 5MWp.

In October 2014, the government shut down the RO subsidy scheme for solar farms larger than 5MWp, citing reasons of affordability due to

the high levels of deployment. The funds provided by city

institutions to invest in solar farms quickly needed to find a new home.

Expect lots of 4.99MWp solar farm projects to immediately

put pressure on the RO budget and don’t be surprised if these also lose RO

support relatively quickly.

But imagine what the entry of these businesses could mean for the

commercial rooftop sector. It’s like

Shane MacGowan, Gerard Depardieu and George Best crashing a genteel party where

the host has already been struggling to keep the punch bowl topped up.

Lightsource alone has allocated £125m fund to the rooftop

sector, perhaps 150MWp of anticipated deployment, and on its own sufficient to

trigger a FIT tariff degression every quarter.

Without changes to its structure of the FIT, this sector could become

victim of its own success. The graph

shows what would happen to the level of the FIT if deployment regularly

exceeded the different degression bands.

If deployment exceeds 130MWp per quarter (a fraction of the hole left in solar farm deployment), the FIT for this tariff band could have reduced by 80% before the end of 2016, so called 'hyper-degression'.

Government promised to 'put rocket boosters' under the mid-scale commercial rooftop sector. Industry has responded, but changes are urgently required to the Feed in Tariff structure to increase the degression limits for the >50kWp band. If we can't get this fixed, then we risk yet another cycle of boom-bust for the industry.